对于如何撰写一份期刊论文进行批判性分析,相信在海外留学的学子们并不陌生,尤其是英国大学的学生,几乎所有的学生都会这样写,那么如何写好这类文章就成了困扰留学生,特别是新生的一大难题。所以,在这里 duewriting论文小编就与您分享一下文献评论文章的写作技巧。

先要了解什么是文献综述。文章综述有时也称为“sourcecritique”,但这并不意味着当学生评价一份期刊时,一定要对其进行否定的批评。学生应认真阅读本文,仔细分析,并对文章做出公正的评价,包括文章所涉及的正面和负面两个方面。为确保批判性分析的实现,学生必须深刻理解文章所要表达的意思。与此同时,您还需要阅读一些其它相关资料,以帮助客观分析目前期刊论文。批判分析是一个复杂的认识过程,它要求学生运用批判的思维方法来公正地评价文章。具体来讲,批判性分析期刊论文需要做到下面几点:

reading the text carefully and understanding it fully

仔细阅读全文并全面理解文章内容

forming objective evaluation of the text (may need to read other sources on similar topics)

对期刊论文进行客观的评价(也许需要同学们阅读其他的材料和类似的主题)

examining each section and addressing the clarity, original approach, quality of research, strengths and weaknesses and the overall value.

检查期刊论文的每部分内容,考虑期刊论文中涉及的清晰新颖的方法 研究质量,优势与劣势,以及期刊论文整体的价值。

providing justifications to your evaluations.

对自己形成的评价进行辩论,提供强有力的辩证理由。

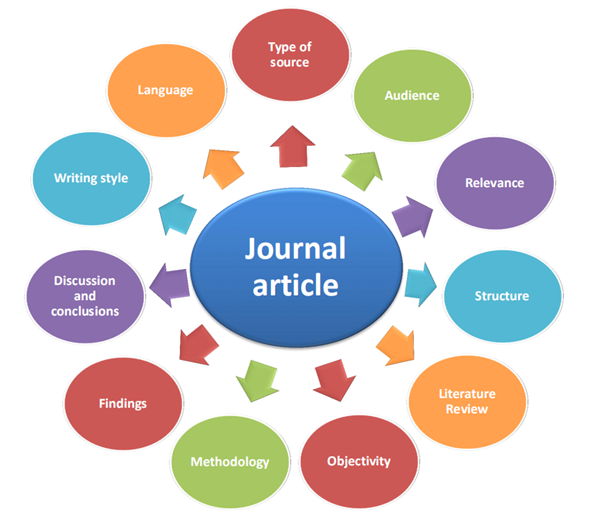

当然,当我们评判一篇journal时,我们可以从以下这些方面讨论(见图1)

了解完什么是文献评论,接下来我们来讨论如何完成一篇critical analysis of a journal article. 在开始阅读文献之前,同学们需要就文献问自己一些问题,以帮助自己更好的理解将要评论的文章,也为了完成一篇更好的文献评论。具体问题如下:

| Full reference Title of the source Type of the source | What is the title of the source? What does it imply? What type of source is it? When was it published? Is it an up-to-date source? |

| Intended audience | What type of reader is the source intended for? Is the source aimed at a specialised or a general audience? Does the source provide basic, advanced, technical or general information? What is the purpose of the source: informative, instructive, persuasive or descriptive? |

| Relevance | What is the topic of the source? Is the source relevant to your essay/module/course? Does the source provide specific enough information or is it too general? |

| Structure | Does the source have an abstract? Is it clear? Does it summarise all sections of the source? How many sections does the source have? Are they clearly indicated? Are the research focus, research aims and objectives clearly stated and justified? |

| Literature Review | Does the source provide completely new information based on primary research or does it repeat information from other sources – secondary research? Are references to other sources evident? Is the literature review well-structured with logical progression of ideas? Has the author used literature relevant to the research aims? Has the author discussed all key areas of the subject in sufficient detail? Has the author provided sufficient evaluative comments on the literature that was discussed? Has the author made any major assumptions? |

| Objectivity | Is the information presented in the source factual or opinion-based? Has the information been well-researched and is it reliable or does it seem to be an opinion unsupported by evidence? Are the author‟s views similar to other writers within the same discipline or are the views profoundly different? If different, a closer critical analysis of the source should be done. Has the author provided equal amount of information for both sides of the argument or is one side more discussed than the other? If so, do you think the author might be biased? What bias can you identify – political, institutional or personal? Are there any pieces of information that have been omitted? If so, why might that be? |

| Methodology Methods Rationale | Has the author clearly stated and justified the methodology, methods? Has the author related (provided a justification) the methodology, methods to the research aims and objectives? Has the author provided sufficient information on the methods and strategies used to carry out the research? Are they clearly explained? Has the author provided clear information on the sample used in his research and has he considered the ethics? Can you observe any issues with the methods/sample/ethical considerations? If yes/no – write about it. What alternative approaches could be suggested to conduct this particular research? Why? Would they provide better results? Has the author clearly stated any limitations of their research? |

| Findings | Has the author clearly described the methods of analysing the data? Has the author clearly presented the results and findings? Are they major or secondary findings? Do they confirm what other authors found out or are they totally different and new? Has the author used any visuals to present the results? Are they clear? Are they the best methods to visualise the results? |

| Discussion and conclusions | Has the data been clearly and sufficiently discussed/ interpreted? Has the author linked their results to the research aims and objectives and the literature review? Has the author provided clear conclusions and are the conclusions based on the findings? |

| Writing style: Logic Emotional language Evidence | Does the author present information in a logical order? Is the text easy to read or is it confusing? Can you clearly identify main points and supporting ideas? Can you easily identify the author‟s central argument – thesis statement? Is that central argument well supported with relevant and sufficient evidence or is it just an opinion? Does the author use any statistics and examples? Are they accurate, can they be checked? |

| Language | Has the author used clear, simple or rather sophisticated, technical and confusing language? Can you find examples of that language? Why do you think the author would use sophisticated, confusing language? Has the author used objective, cautious language (may, can, might, etc.) or have they used emotional (extremely, amazing, etc.) and very definite (something definitely is, I know something for sure, etc.) language? |

| Critical reviews | Has this source been critically peer reviewed? Are the reviews positive? Do reviewers/critics have the same opinion about the source or is there a debate among them? |

带着这些问题读完需要批判性分析的文献,相信同学们对此文献应该有了一个深入的理解。接下来,就需要开始critical analysis of a journal article的写作。当然,这里同学们最好遵循期刊的结构和标题,这样可以帮助同学们客观评价文章的所有章节。此外,当同学们在阅读文献的时候,最好在文献上做一些批注,然后根据在文献上的批注,列出文献评论文章的结构。这里,同学们就需要回顾上述列表中的问题,保证你论文的结构和主要观点符合逻辑顺序。最后同学们可以根据下述结构,开始自己critical analysis of a journal article的写作。

Introduction(First paragraph):

- Information about the author, title of the article, type of source

- Intended audience and the purpose of the source

- Topic and the relevance of the source

- Abstract and structure of the article

Main body section:

- Literature Review

- Objectivity

- Methodology

- Findings

- Discussion and conclusions

- Writing style

- Language

- Critical reviews

- Comparison to another source (only if asked to do)

Conclusion:

- Summary of your analysis

当你完成第一稿后,你需要认真的进行检查,包括语法,词汇,标点,拼写,观点组织和文本内引用。有一点需要注意的是,当你做critical review of a journal article时, 你要确保你的观点合乎逻辑,避免重复。如果你需要重复一些观点,尽量用不同的方式来表达这些观点—可以利用同义词或者改写等。

上述是duewriting论文小编对如何写critical analysis of journal article的一些建议,同学们看到这里也许会似懂非懂的。什么也不多,给大家一个具体的例子,帮助同学们更好的理解和消化duewriting论文小编在上述文章中提到的写作技巧和步骤:

Critical Analysis of a Research Paper

Towards an integrated contingency framework for MAS sophistication

Case studies on the scope of accounting instruments in Dutch power and gas companies

Title

The title suggests that the article will give guidance towards a contingency framework for MAS sophistication. The Contingency framework states that there is no one right way to manage an organisation, so the part “towards integrated […] framework” with the word “contingency” seems like a paradox. We feel that we might not have chosen this article if we were looking at the title only because it seemingly contradicts itself.

The group agreed that the title is quite long. We have analysed it by defining the main words of which we used the Macmillan Dictionary (2002) (See appendix B).

After understanding the words and theory explanation, the title became quite easy to understand.

Abstract and Introduction

We feel that the abstract provides concise and simple information. It is a good explanation and expansion of the title. We have chosen this article because it can be easily understood. The abstract states that many companies are being convinced to implement newly developed management accounting systems and also comments on its inappropriateness. The author states the reason for this is due to the contingency theory perspective. She also highlights that this article is based on the cases of two power and gas companies.

The introduction is interesting and very informative. It lays out very clearly what the author will discuss by dividing the article into sections and also talks about the „sophisticated‟ techniques such as ABC. She also identifies that the causes and criticism of MAS sophistication is due to the methodology of research undertaken in previous years like the cross sectional survey method.

With this mind, Tillema (2005) says that she will try to overcome the weaknesses by using different approaches of research.

This article relates to Management Accounting Systems and its instruments, contingency theory and two case companies. It is divided into 5 main sections, which helps with the reading because it is very long.

The author is an academic staff member of the Faculty of Economics at the University of Groningen, from which she graduated. She is an assistant professor in finance and management accounting and is involved in the university‟s management accounting and finance courses. Her main focus for researches is a wide area of management accounting (University of Groningen, no date).

We think that she knows the topic very well considering she teaches Management Accounting at the University. The research that she undertakes is convincingly reliable which we think is highly significant and logical as her main focus is on management accounting.

Critical Analysis

We believe that the main issue of this article is the inappropriate implementation of the MAS without taking into account the contingency theory. The author mentions that researchers found out that the introduction of sophisticated accounting techniques was often unsuccessful due to the lack of consideration of various contingent variables. It seems that managers want to find the best way to make their specific company successful when implementing new MAS‟s. We agreed that the sophisticated techniques are dependent on the environment in which they are used and this is where contingency theory becomes very important. We think that the article highlights the problem really well and feel it is a good pointer in dealing with the contingency framework and the scope of accounting information.

Every business may introduce different accounting techniques at various levels of sophistication. Hence the need for contingent approaches i.e. what suits the organisation? This paper identifies the contingent factors for the sophistication of accounting instruments in two Dutch companies.

In addition, the author tries to answer three questions: “Which contingency factors influence the scope of accounting instruments? […] How these contingency factors interact with each other and with the various characteristic of organisations and their environment? […] Which mechanisms explain the scope of accounting instruments?” We think that the author writes the article answering the three questions whilst explaining her findings which she summarises really well.

The author‟s intention is to improve awareness about contingency theory by describing its factors with reference to the two case studies. We think that the target audience are all people interested in management accounting as well as students.

Research

We think that the author has provided a research framework in a positive way because it is highly detailed and could be helpful in guiding further research. This framework was planned in three stages.

In the first stage, the author used the two largest Dutch power and gas companies to support her study. Here, she mentioned that her main reason were changes in the scope of accounting instruments in a short period of time within the companies. The change of accounting instruments used occurred respectively with regard to the company‟s structures.

In the second stage, she collected data through interviews. The data were then compared for verification to the data from document analysis which we think is a better research method.

compared to sending postal questionnaires. The process of the interview was well carried out in the sense that the accountant of a specific department was interviewed before the managing director of that department.

The final stage was data analysis which was done in two stages: the first was within-case analysis and the second cross-case analysis. Each within-case analysis started by sorting out the case company‟s past, current and future accounting instrument regarding their scope. We all agreed that the method used for the research was efficient and substantial.

Results

The result from the empirical research indicates that nine contingency factors have a direct influence on the scope of accounting instruments. The author relates the existence of contingency factors (appendix C) with different level of the organisation (beyond-organisation, organisation and sub-units, operating task, accounting tasks).

Beyond the organisational level, the author revealed that regulations, accounting innovations and trends will influence the scope of accounting instruments used by organisations. She supported this assertion by defining the adoption of management accounting techniques such as balance score card, the economic value added activity and shareholders‟ value. However, we feel that it would have been very helpful if the author tells us in this paper the effects of the adoption of these instruments on the performance of those Dutch companies and support them with some financial data.

The author relates the two Dutch companies with willingness or potential willingness to embrace broader accounting instruments by their shift from a more focus on “implicit non-financial measure” (Tillema, 2005) to a more financial performance related behaviour. Here we feel that the author is trying to convince us that the change of a company financial objective should always be followed by its shift to the accounting instruments used. We can justify this statement on the basis of the two case studies.

At the operating task level, the author defined the visibility of financial consequences of the operating task as a factor that influences the scope of accounting instruments. This is because it gives detailed information on the cost incurred with the activities of those companies.

With regard to the complexity of operating tasks, the author thinks that it may, in certain circumstance, be subjective to influence the scope of accounting instruments. For instance cost- benefit analysis may imply the use of average or broad accounting instruments whereas restricting costs or expenditures may imply the use of narrow accounting instruments (Tillema, 2005). In addition, we understand from the case that in the dynamic environment, acceptable forecast of the future financial situation requires investigations of the financial consequences on the possible future market circumstances. Another example is that the case companies introduced several broad scope instruments since their environments have become far more dynamic. This was due to the liberalisation of the energy market and the introduction of external telecommunications products.

At the accounting task level, the empirical research revealed two factors as direct consequences of the type of accounting instruments used in the companies‟ accounting instruments. These factors are: the significance of accounting instruments and the clarity of accounting instruments. According to the author one of the case companies‟ that is concerned with only energy supply experienced low cost in its decision making which was done in a low frequency base using narrow accounting instruments. Moreover the author related the use of this narrow accounting instrument in the event of uncertainty of financial consequences of a decision.

The author informs us only about some facts related to the case companies. It would be better to have some practical examples on the financial performance of the companies. It would support managers when making decisions in the future.

Conclusion and Discussion

We think that the conclusion is pretty much straight to the point defining outcomes of the research. She answers well, in our opinion, all three questions from the introduction. She says that scope of accounting instruments is influenced by many of the contingency factors and there are few factors, which communicate with institutional context of these instruments.

The author recognised that the other research methods used in other case studies i.e. (cross sectional) are considered as inadequate by academics but has produced one consistent variable (dynamism of the environment). We think this is an important factor as other research has proved this to be a common factor including the comparison article by Abdel-Kadera and Luther (2008).

This article based on two case studies shown “the relationship between a known contingency factor and the scope of MAS” (Tillema, 2005).

As a group, we thought this article has been written with precision having carried out extensive research and taken into consideration other factors like the mindset of managers and accountants with personal face to face interviews.

The author suggests areas of improvement and also gives own recommendations on her article. She suggests how her research paper could be improved by investigating whether the contingency framework developed in this paper is useful in explaining the scope of the accounting instruments of organisations that were not included in the empirical research. We could not agree more with this statement because by doing so, it enriches the article and adds more substance to it. Evidently, this has been carried out in the comparison article; here they carry out the research on the food and drinks Industry.

Another suggestion she makes is to find contingency factors at the individual level of analysis.

Overall, a very good article, it covers a lot of factors and explains the points concisely based on extensive research and case studies about the sophistication of MAS in relation to contingency theory. Not only does the article do this well but the author also recommends ways in which it could be better understood.

Comparison to another article

„The Impact of Firm Characteristics on Management Accounting Practices: A UK-based Empirical Analysis‟ by Abdel-Kadera and Luther (2008) is the article we have chosen for comparison.

This article was chosen because the topics are similar. It attempts to explain why firms adopt different management accounting techniques, particularly in the UK. The article by Tillema (2005) has also been referenced in support to their article because it explains same issues in relation to the contingency theory and management accounting sophistication. It is a more recent version compared to the article by Tillema (2005) and also looks at a different type of manufacturing industry.

This article uses empirical research meaning the data is based on experiments and observation as well as interviews much like Tillema (2005) did. However, we think there is a weakness in the way the research was conducted. Much of the empirical data was done through postal questionnaires and a limited number of face to face interviews were carried out (Abdel-Kadera and Luther, 2008). Whereas Tillema research methodology is more efficient and gives a better view on the various aspects of difference in management accounting practises; it is precise and more accurate.

Both articles come to a conclusion that difference arise in management accounting practises and MA sophistication because of the external environment and operating activities. Abdel-Kadera and Luther go further by stating that customer power, decentralisation and size also affect the accounting practices. (Appendix A)

We feel that the article by Tillema is very evident and well researched. It has an edge over this article and that is why she has been referenced extensively. We also think that both articles have a common conclusion with slight differences and additions being made in this article.

Appendix A

Appendix B

Towards: nearer to a particular result used for showing how a process is developing in a way that will produce a particular result

Integrated: combining things, people, or ideas of different types in one effective unit, group, or system

Sophistication:the quality of knowing and understanding a lot about a complicated subject Scope: the things that a particular activity, organisation or subject deals with

Appendix C

Contingency factors:

Accounting innovations and trends

regulations,

importance of financial objectives,

interaction between organization and organizational parts,

the visibility of operating task,

the complexity of operating task,

the dynamism of the environments,

The significances of financial consequences

the clarity of financial consequences

References

Abdel-Kader, M., & Luther, R. (2008). The impact of firm characteristics on management accounting practices: A UK-based empirical analysis. The British Accounting Review, 40(1), 2-27. doi:10.1016/j.bar.2007.11.003

Kaplan, R.S. (1986). Accounting lag: The obsolescence of Cost Accounting Systems. Boston: Harvard Business School Press.

Rundell, M. (2007). Macmillan English dictionary for Advanced Learners. Oxford: Macmillan.

Tillema, S. (2005). Towards an integrated contingency framework from MAS sophistication: Case studies on the scope of accounting instruments in Dutch power and gas companies. Management Accounting Research, 16(1), 101.

原创文章,作者:duewriting,如若转载,请注明出处:https://www.duewriting.com/93.html